NVIDIA’s 2026 State of AI report reads like a victory lap. Eighty-eight percent of enterprise leaders say AI increased revenue. Eighty-seven percent report cost reductions. Eighty-six percent are growing their AI budgets this year. If you stopped there — and most of the coverage did — you’d conclude that enterprise AI has crossed every finish line that matters.

But buried in page after page of bullish data from 3,200 enterprise leaders is a finding that should give every CFO pause: 30% of those same leaders admit they still can’t quantify the ROI of their AI investments. Nearly one in three organizations spending more on AI this year cannot say, with any rigor, whether last year’s spending worked.

Source: All data in this analysis comes from NVIDIA’s 2026 State of AI Report, a survey of 3,200+ enterprise leaders across six industries conducted August–December 2025. Charts reproduced from the original report.

The Headline Numbers vs. the Fine Print

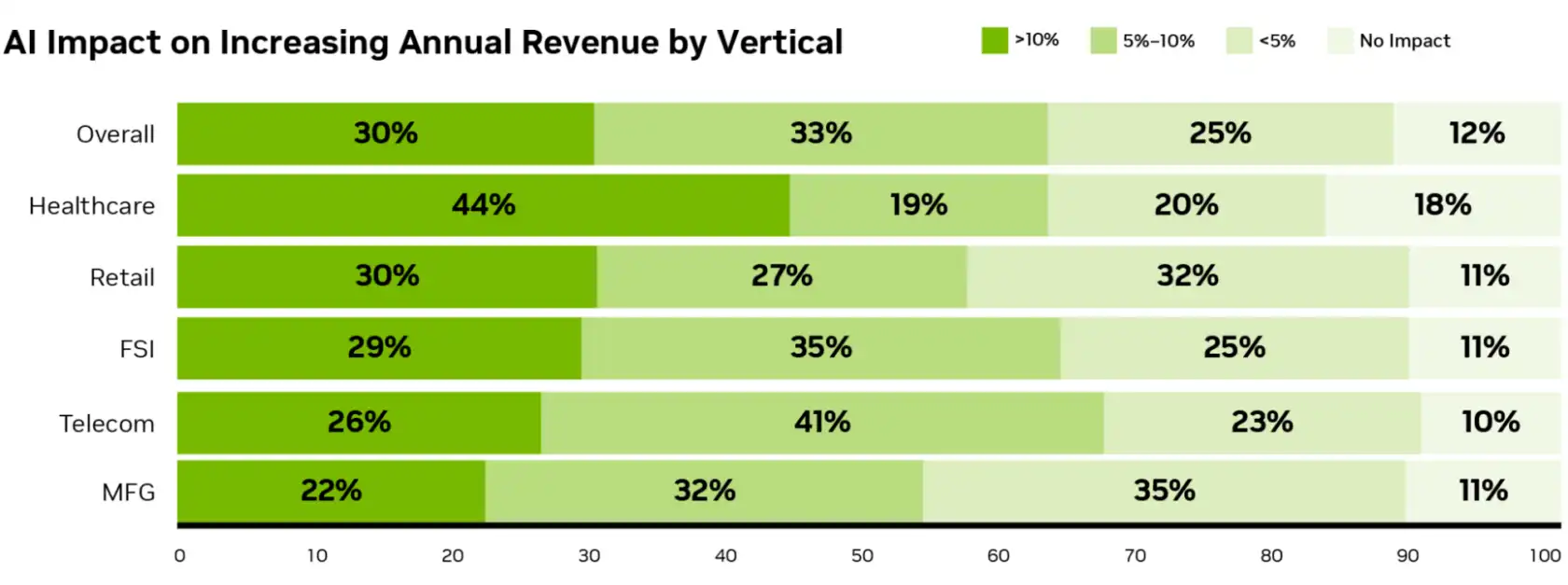

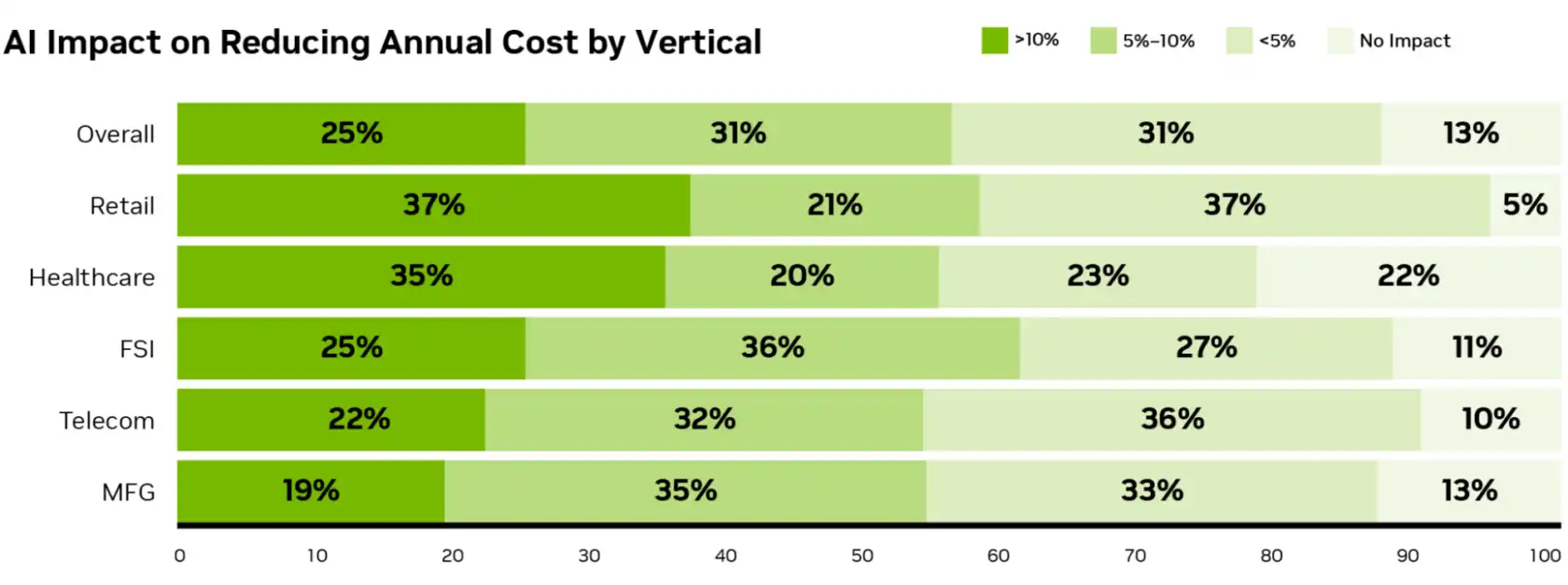

The optimistic numbers are real, and they’re striking. Among the 3,200+ respondents surveyed between August and December 2025, 30% reported revenue increases exceeding 10%, with another 33% seeing gains between 5% and 10%. Cost reductions were nearly as widespread — 87% reported savings, and a quarter achieved cuts greater than 10%. In retail and consumer packaged goods, that figure climbed to 37%. These aren’t pilot results. They’re self-reported impacts from organizations with active AI deployments across financial services, healthcare, manufacturing, telecommunications, and retail.

The trouble is how those numbers were generated. Self-reported revenue impact and measured revenue impact are different things. When NVIDIA’s own survey shows that 48% of respondents struggle with data sufficiency, 38% lack the AI expertise they need, and 30% can’t quantify ROI at all, you have to ask: how confident are the other 70% in their numbers? The report doesn’t say. And that gap between perception and measurement is where billions of dollars in AI spending disappear every year.

This isn’t a reason to dismiss the progress. Organizations like PepsiCo, which achieved a 20% throughput increase and 10-15% reduction in capital expenditure through AI-powered digital twins, demonstrate that AI can deliver measurable returns. Clinomic’s medical ICU assistant reduced documentation errors by 68% and clinical workload by 33%. These are concrete, instrumented outcomes. The question is why so many organizations can’t produce similar evidence.

The Measurement Problem Gets More Expensive Every Quarter

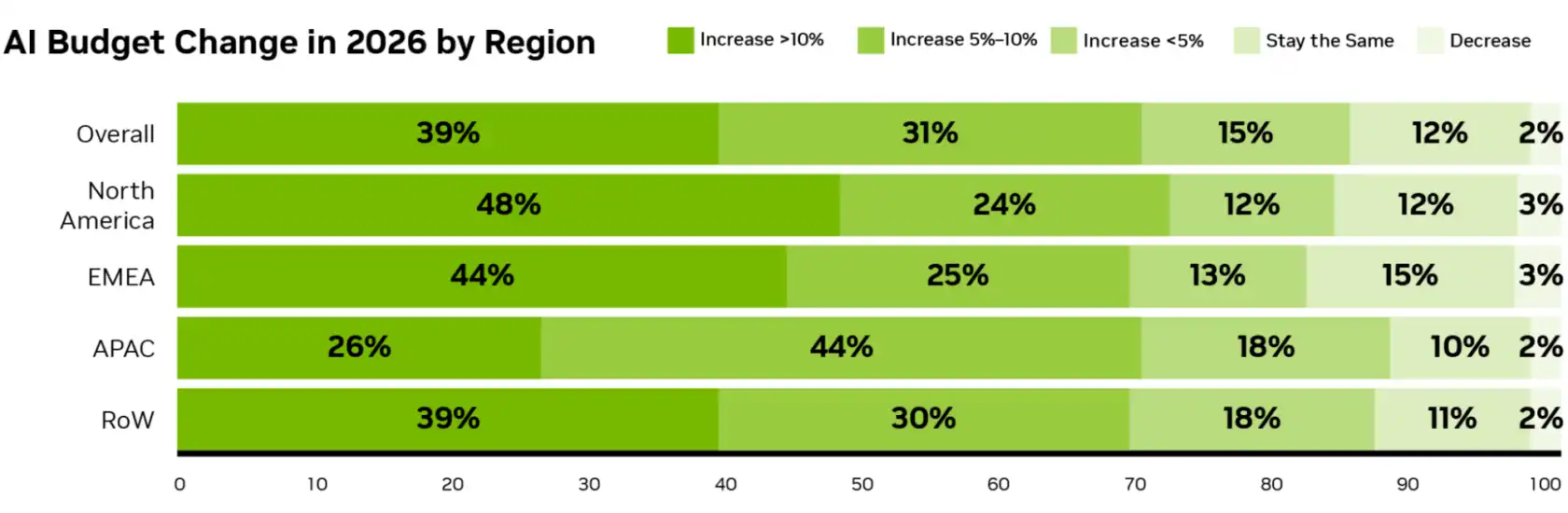

Budget season makes the stakes concrete. Eighty-six percent of organizations are increasing AI budgets in 2026, with 40% planning increases of 10% or more. North American enterprises are even more aggressive — 48% are pushing budgets up by double digits. These aren’t exploratory budgets. They’re operational commitments that will demand operational proof.

The organizations that instrumented early have a structural advantage. Lowe’s built AI digital twins for more than 1,750 stores and can point to the cost of generating 3D product models — under $1 each — as a clear efficiency metric. Nasdaq constructed a proprietary AI platform and can trace its impact across both internal operations and external products. These companies didn’t stumble into measurement. They designed for it from the start, choosing specific outcomes to track before deploying the technology.

The 30% without measurement infrastructure face a different budget conversation entirely. When the CFO asks what last quarter’s AI spend produced, “we believe it’s helping” isn’t an answer that protects next quarter’s allocation. As AI budgets grow, the metrics that matter to financial leadership become non-negotiable — and organizations without baselines can’t even begin that conversation.

Agentic AI Makes the Gap Worse

Perhaps the most forward-looking finding in the report: 44% of organizations are already deploying or actively assessing AI agents, with telecommunications (48%) and retail (47%) leading adoption. These aren’t chatbots answering customer questions. Agentic AI systems operate autonomously — making decisions, executing multi-step workflows, and interacting with other systems without human approval at every stage.

That autonomy creates a measurement blind spot that assistive AI never did. When a human uses ChatGPT to draft an email, the value chain is short and visible. When an AI agent autonomously triages customer issues, escalates edge cases, updates CRM records, and triggers follow-up workflows, the value chain branches and compounds in ways that are nearly impossible to track without purpose-built instrumentation. If 30% of organizations can’t measure ROI on their existing AI tools, they’re not going to suddenly develop that capability for systems that are orders of magnitude more complex. Every autonomous decision an agent makes without measurement infrastructure is both an ROI blind spot and a risk exposure.

What the Winners Did Differently

A pattern emerges when you study the case studies NVIDIA highlights. PepsiCo didn’t deploy digital twins and hope for the best — they defined throughput improvement and capital expenditure reduction as target metrics before writing a line of code. Clinomic didn’t build a medical assistant and then try to figure out if it worked — they instrumented documentation error rates and clinician workload from day one. Lowe’s didn’t scale to 1,750 stores on intuition — they tracked cost-per-model as a unit economic that justified each expansion.

The 30% who can’t quantify ROI didn’t fail at AI. They failed at instrumentation. They deployed capable technology without building the measurement layer that turns activity into evidence. And now, with budgets growing and boards asking harder questions, that gap is becoming a strategic liability. McKinsey’s latest research echoes this finding — organizations that establish clear performance metrics before scaling AI are significantly more likely to capture value across multiple business functions.

The framework that separates measurement leaders from the rest follows a consistent pattern: first, establish visibility into what AI is actually doing across the organization; then, define the business metrics that matter for each use case; next, run structured evaluations against those baselines; and finally, use the evidence to make scale-or-sunset decisions. This See-Measure-Decide-Act cycle is what transforms AI investment from a faith-based initiative into a data-driven program.

What to Do Before Your Next Budget Review

The NVIDIA report makes one thing clear: the AI investment wave is not slowing down. With 86% of organizations increasing budgets and 44% moving into agentic AI, the volume of spending that needs justification is only growing. The organizations that thrive in this environment won’t be the ones with the most sophisticated models or the largest GPU clusters. They’ll be the ones that can answer, with precision, what their AI investments produced.

If you’re in the 30% today, the path forward isn’t complicated — but it is urgent. Instrument before you scale. Establish baselines before your next deployment. Build measurement into your AI architecture the same way you’d build security into your cloud infrastructure: not as an afterthought, but as a foundational layer. The CFO will ask for proof. The board will ask for proof. Make sure you have it.

Ready to close the measurement gap? Schedule a demo to see how Olakai gives you unified visibility, business-aligned KPIs, and ROI evidence across every AI tool in your enterprise.